1. Usage scenarios

If you anticipate that the stock price will fluctuate significantly in the future, but are unsure whether it will rise or fall, you can use the buying cross-portfolio strategy.

2. How to build

Long a wide-span portfolio consists of two options trades:

● Long call

● Long put

Call's exercise price > put's exercise price, and the underlying stock, quantity, and expiration date of call and put are all the same.

3. Strategy brief

Long a wide span combination generally consists of buying calls and puts for the same target, quantity, and fictitious value of the expiration date.

To buy calls and puts at the beginning of establishing this strategy, you need to spend option premium. If the stock price rises sharply, the profit is obtained by holding the call; if the stock price falls sharply, the profit is obtained by holding the PUT.

Regardless of whether it rises or falls, as long as the increase or decline is large enough so that the return is greater than the option premium paid, you can make a profit.

Buying a wide-span portfolio is very similar to buying a cross-span portfolio. The only difference is that buying a wide-span portfolio is generally composed of imaginary options, so the construction cost is lower than buying a cross-span portfolio, but in line with this, if you want to make a profit, the underlying asset required to buy a wide-span portfolio also fluctuates more widely.

Other than that, the characteristics of buying a wide-span combination are almost the same as the characteristics of buying a cross-span combination:

● Strategy losses are limited, and potential profits are limitless. The biggest loss of this strategy is the cost of buying options. The unlimited potential profit is due to the possibility of unlimited profit from buying the call portion.

● The strategy does not depend on the direction of future changes in the stock market price. Buy call is bullish, buy put is bearish. The different exercise prices of the two options hedge against directionality within a certain price range.

● Time decay is bad for strategy. Time decay is not good for option buyers, and is one of the characteristics of options. Investors who buy wide-span portfolios are pure option buyers, and time decay is naturally disadvantageous.

● Buying broad-span portfolios is a strategy to increase volatility. Investors using this strategy can not predict whether stocks will rise or fall, but it must be based on the expectation that "stocks will fluctuate significantly in the future", that is, they are optimistic about future market volatility.

Judging from the impact of volatility on option prices alone, when market volatility rises, option prices will rise. Conversely, future market volatility decreases, making it suitable for selling options.

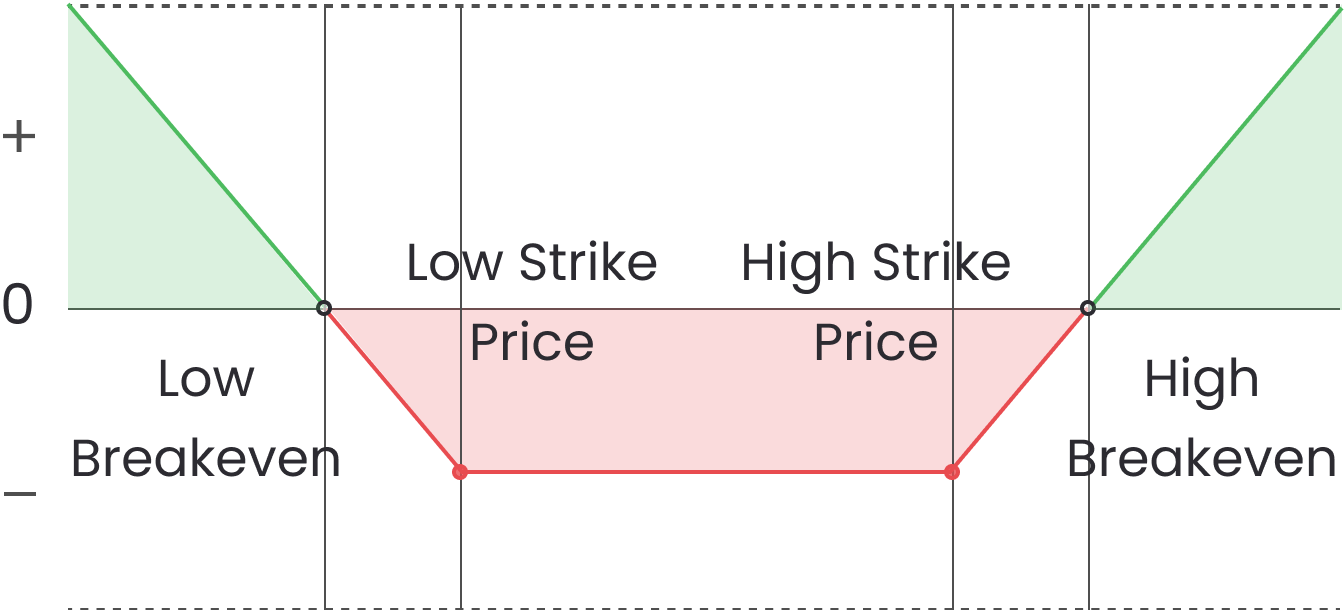

4. Risk and Return

P/L:

Max Profit: Unlimited

Max Loss: Purchase Cost

Breakeven:

High Breakeven: High Strike Price + Purchase Cost

Low Breakeven: Low Strike Price - Purchase Cost

P/L Calculation Formula:

tock Price >= High Strike Price: Stock Price - High Strike Price - Purchase Cost

Low Strike Price <= Stock Price < High Strike Price: - Purchase Cost

Stock Price < Low Strike Price: Low Strike Price - Stock Price - Purchase Cost

How To Make Profit?

Stock Price < Low Breakeven Price

Stock Price > High Breakeven Price

5. P/L Chart